How do you equate investors anticipating a recession with being overly optimistic?

How do you equate investors anticipating a recession with being overly optimistic?

MarketWatch wrote:

"Economic data, including readings on consumer confidence and home prices, were mostly positive.

Investors are looking ahead to important readings on inflation, durable-goods orders and a second estimate of fourth-quarter GDP, expected later this week.

After a rocky start to the year, U.S. data has improved over the past two weeks. Stronger-than-expecting readings on retails-sales growth and consumer-price inflation bolstered the case for at least one Federal Reserve interest-rate increase this year, analysts said.

"Considering that there's probably a fair number of investors who are anticipating a recession, I believe that good news will be good news for stocks, considering where investor sentiment is currently situated," said Jack Ablin, chief investment officer at BMO Private Bank."

WTF is this bullshxt? Is it from Marketwatch?

THIS is from Marketwatch, 23 Feb 2016: "Consumer confidence falls to seven-month low"

http://www.marketwatch.com/story/consumer-confidence-falls-to-seven-month-low-2016-02-23and from 28 Jan 2016: "Orders for durable, or long-lasting, goods fell 5.1% in December, the Commerce Department said Thursday"

http://www.marketwatch.com/story/durable-goods-orders-slide-51-in-december-2016-01-28The only "up" news was certain types of housing in certain areas--and even at that, some credible commenters believe the US residential RE market to be overvalued to the tune of 25-40%, something which which I agree, depending on location.

"Investment firms are not anticipating a recession and investors are overly optimistic, this will be doubly bad for stocks, and that is why stocks are going down today, and oil is down too. That explains it all in a nutshell, for those that want an easy answer to complex financial markets." says Igy.

Aren't those government numbers? I thought you didn't trust those, or is that only when they don't fit your narrative?

Maserati,

We have had a wave of posters that quote this B.S.. So I am having fun of making a parody of their nonsense.

Igy

Sally V wrote:

Aren't those government numbers? I thought you didn't trust those, or is that only when they don't fit your narrative?

It is obvious to those who cognate that I was opining not on the accuracy or intrinsic meaning of the numbers, but on either the inconsistency of Marketwatch, or the accuracy of the quote to which I responded.

Try to keep up, Sally. Stop trying to take pot-shots, you suck at it, as do all similar inferiority-complex-riddled posters.

How about commenting on Basel II and AT1 and T2 capital as they relate to CoCos?

I thought not.

Get your hand out of your pants, close the porn windows you obviously have open, and grow up.

Maserati,

Good one, she deserves it.

Google JPM, it goes along with your Deutsche Bank thesis. They are increasing their provisioning for bad energy loans by more than 60%. Confessionals are coming.

Igy

Yes I saw that. The potential problem comes when government steps in, or pumps a secondary market, in which these instruments are aggregated, tranched, and essentially re-valued, with the gov't doing things like changing accounting rules so that somebody will underwrite the issuance, if not the gov't itself doing it.

I don't think this group of loans is large enough at JPM to warrant any significant intervention, but we will see. I am somewhat confident that those at DB are much larger, and much more troublesome. Let the salesmanship begin!

JPM energy loans: http://fortune.com/2016/02/23/jpmorgan-oil-losses-loans/

Maserati,

If the loan losses hit $3 billion that will be a hit to earnings. Financial sector down over 10% so the infection is probably more severe than what is currently in the market. And as confessionals come out it looks to be a further drag to S&P 500 earnings. That is one reason you cannot say the problem is just energy or commodities, it cannot be isolated so easily.

Igy

The previous two posts using my name were authored by an imposter. I do not belittle or denigrate the opinions of others. I will on occasion respectfully disagree.

I will be taking a respite from this thread until the troll tires of his childish ways.

The 12-year-old is busy trolling again under my name. Incredible.

I'm out again for the day.

Ghost of Igloi wrote:

JPM energy loans:

http://fortune.com/2016/02/23/jpmorgan-oil-losses-loans/

Igy,

That's not even the tip of the iceberg. First you have to add in, not just energy loans but commodity loans, for things like copper mine production in South America, gold mine production at places like Anglo American....

And if you add all that up, you now have the TIP of the ICEBERG.

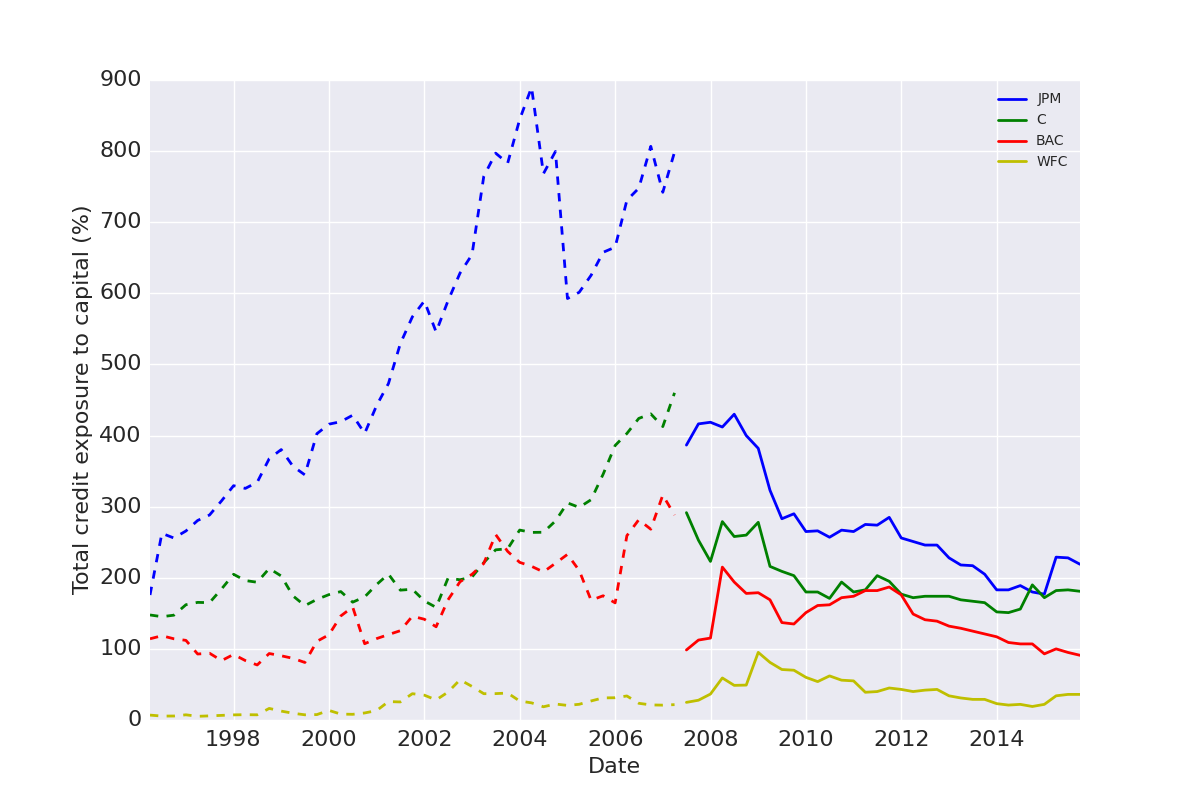

THIS is the iceberg. This is all the nuclear waste over the counter derivative exposure still on the books of big banks (this is percent of total capital) from 2008:

https://staticseekingalpha.a.ssl.fastly.net/uploads/2016/1/9/6425571-14523863394774084-Sebastien-Couvidat_origin.pngYou may now say, "Holy Shit." If they have big enough losses from energy loans that they can't cover this nuclear waste, all hell is going to break loose in the money center banks. If you wondered why I'm short most of these guys, now you know.

But thus far, the contagion from commodity and finance to the general market is minimal.

coach d,

You have to ask yourself why are they dribbling this out? There is a pattern there, when issues are far greater than they appear. I have never believed we were totally behind the problems of 2008, only masked by the liquidity. Contagion is hard to put a finger to early on and may have a way to go before the "a ha" moment.

Igy

Igy,

What makes you think they are dribbling anything out? You need to know something about the markets to even know what to search for, but if you do know what to search for, you might not like what you find.

The regulation of clearing of over the counter (read: unregulated) swaps has changed substantially due to Dodd-Frank, but under the Commodity Futures Modernization Act of 2000 (aka, the "Enron Loophole"), derivatives between "sophisticated parties" were changed to being unregulated, and Senator Phil Graham and his wife, who was Chair of the Commodity Futures Trading Commission, were bound and determined to keep these swaps totally unregulated. This is how you ended up with the situation with companies in 2008 betting on the demise of their competitors, then selling their stocks short, and at the bottom in 2009, there was more over the counter derivative exposure than there was money (and that's not cash, but money including central bank assets) in the entire world to cover it.

Since there was NO WAY to cover the derivative risk (because there wasn't enough money to cover it), it is still on the true books of the money center banks, but as off-the-balance-sheet items. This is the ultimate in non-GAAP accounting: Pandora's box hiding in the back of the office. And if you think this is all there is to worry about, this is the iceberg sitting in China:

These things are clearly ticking bombs that could blow up the entire world financial system....and gold won't save you if there is no money to pay for it. We just have to hope the central bankers can keep the current commodity bubble from lighting the fuse.....

coach d,

I have no argument with your analysis of the derivative book size or China's bank debt. My comment about dribbling out information was Jamie Dimon's underplay of the JPM energy loan risk and his purchase of JPM stock when the market was under pressure several weeks ago. Low and behold today with the market and his stock higher releases information on a larger loan loss provision, something I can assume he had information on several weeks ago.

Igy

Igy,

I remember something like 20 years ago, when there was a very well known fund called Mutual Shares, and the manager of said fund had a long interview with Barrons, in which he gave a very positive review of Micron Technology in your area. It turns out that he was using this as an opportunity to unload his entire position in Micron, which Barrons did report about 4 months later (after presumably a certain number of fools and their money was parted). Nothing ever happened to him in terms of legal charges.

Unfortunately, this kind of crap goes on all the time. Pity the poor Justice Department prosecutors that have to go after a guy like Diamond: Their 100% conviction rates might suffer. But they did protect us from Martha Stewart.

Personally, I'm far more concerned about something like $10 trillion in toxic debt floating around the financial universe. As I've said before, don't worry so much about the asset bubble we may or may not have a couple or more years in the future; Worry about the one we've got NOW.

Sally V wrote:

Aren't those government numbers? I thought you didn't trust those, or is that only when they don't fit your narrative?

Maserati wrote:

Try to keep up, Sally. Stop trying to take pot-shots, you suck at it, as do all similar inferiority-complex-riddled posters.

Get your hand out of your pants, close the porn windows you obviously have open, and grow up.

Ghost of Igloi wrote:

Maserati,

Good one, she deserves it.

Igy

Nice job, Maserati and Igy. You guys must be very proud of yourselves.

As pure as fresh snow, Sall V: "At least you realize that your full of shit."

Read more:

http://www.letsrun.com/forum/flat_read.php?thread=5369837&page=487#ixzz41669rBsi

coach d: yes. absolutely.

The problem with toxic assets is the name--toxic. It is a label that is applied to disguise the fact that they represent activities/endeavors/transactions that are not economically viable.

The lack of regulation exists in order that the values may be fudged, to make them seem better, when they're not. Essentially, such assets (and now bonds) were fictionally valued, as were their derivatives, to make them seem economically viable.

Then, money was made really cheap so that institutions, etc. could go out and buy these things--that, AND the government went and bought a whole bunch of it, to "lead the way".

Meanwhile, the activity/endeavor/transaction was still not economically viable, even when accounting rules were changed. Accounting is NOT economics.

In the intervening years, even though TARP assets have been sold, this type of activity has not only continued, it has increased tremendously--and of course you are correct in pointing out that they are off-balance-sheet items.

Nothing worthwhile net is being added to civilization by these activities; they do not add more than they cost, which costs appear as dilution. They are not worth their fictitious valuations. To make it SEEM like they are, money has been made cheap, and rules changed, and we got asset inflation, which has also affected equities and bonds.

One cannot merely stand still, or one will be diluted to death.

This is why I find fundamentals important. While technicals describe the aggregate behavior of market participants (the subject of the market), fundamentals can describe the economic qualities of business endeavor (the object of the market). Both can be important to use, at various points in cycle timing, IMO.

{kind=link}