Biden came out and said what he said to stem the contagion you mention. Still doesn't help a few root causes:

1. The worthless paper SVB had on their books were Federal Treasuries which are generally termed as "risk free". Spoiler: they aren't. Because...

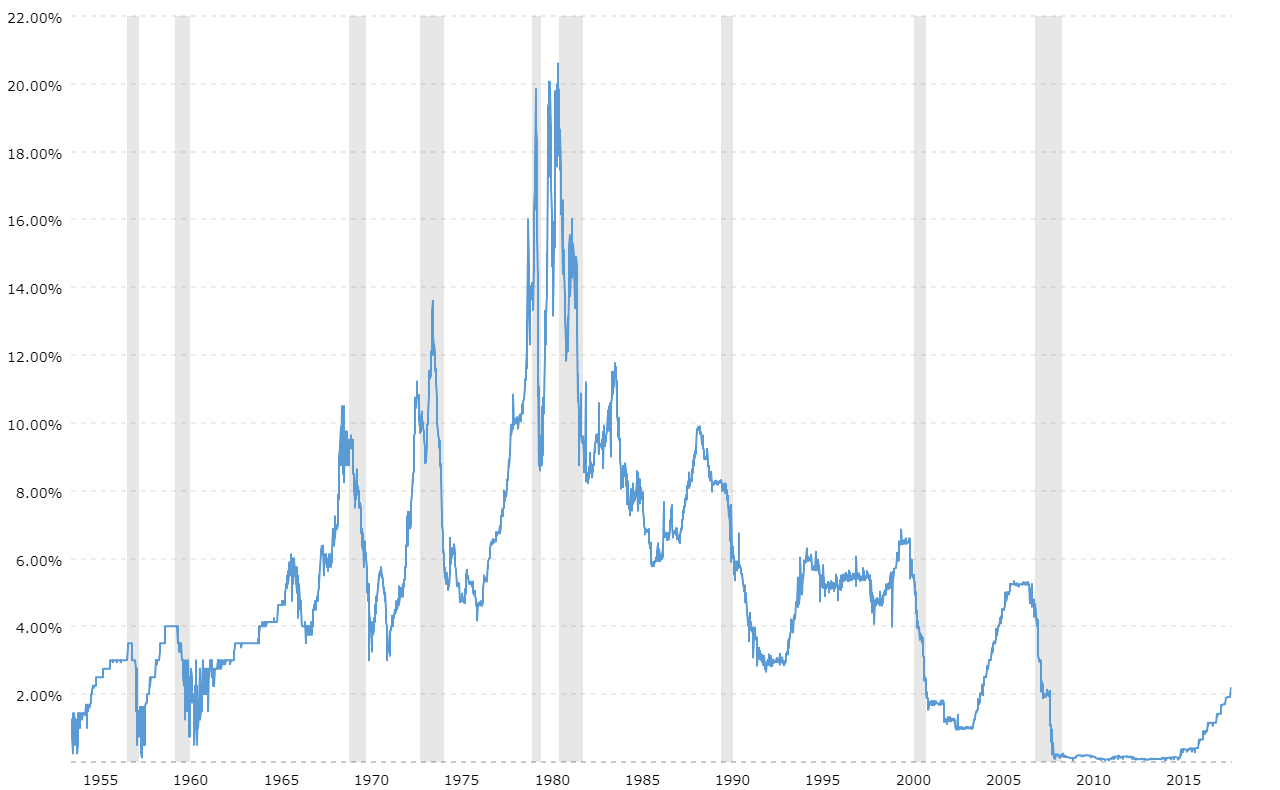

2. Fed raised rates too quickly, causing the Bonds to become worthless. Because...

3. Fed/Biden had the blinders on regarding Covid inflation. They reacted too slowly and were in complete denial. Using words like "transitive" or "temporary"

So again, Fed has raised rates through open market operations, decreasing M1 supply. Now banks own the worthless paper and can't cover demand deposit accts due to high rates, decreased money supply and bonds they can't liquidate because they aren't worth anything.

Lot of this is the fault of the current administration.

/cloudfront-us-east-2.images.arcpublishing.com/reuters/ICCQYDORC5OALAHSAJEDCYIEVE.jpg)

-min.png)