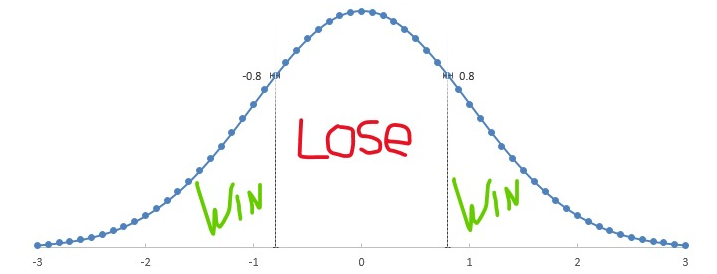

For anyone tired of agip posting predictions of "market gurus" that were wrong or right, I am offering an alternative. Why not keep track of cumulative market sentiment of people with skin in the game? This is expressed in the options market, specifically $SPX. This is an European option, settled on a cash basis and can only be exercised at expiration. I posted some stuff a while back by Kris Abdelmessih at Moontower. He discusses straddles and I will use at-the -money ( or close to them; as well as an approximation using his formula ) straddles from Barchart and Optionsprofitcalculator.com.

As of 3/21/2024; $SPX 5675 straddle for 12/31/2025:

Barchart - BE 6369.70 (+12.4%) and 4980.30 (-12.1%) Net Debit is $694.70

OPC - BE 6366.60 (+12.33) and 4983.40 (-12.1) Net Debit is $691.60 BC uses ask price and OPC uses mid.

Using Moontower's formula, Net Debit is 670.48 (+or- 11.83%).*

BEs are 6338.04 and 4997.08

Keep in mind 3/21/2025 close was 5667.56. The IV is 16.62% and the HV (Historical Vol) is 17.48%. 12/31/2024's close was 5881.63 and the yearly high was 6144.15 on 2/19/2025

I will update this not every week but at least once a month until 12/31/2025.

*Using HV and MT formula Net Debit would be $792.55!