And yet you seem pretty certain of the coming effects of the upcoming election on markets? Maybe you think you CAN have your cake and eat it too…

Oh I'm not pretty certain of anything.

I do think it's possible to reduce risk though, at the cost of potential return. That's what I'm doing...taking some chips I won off the table. Not a prediction so much as a risk control. I'm fine if I don't make as much as I could have.

1) The market isn't going to drop 50% in the next 10 years.

2) If it did, I would still have way more than enough. Not only do I just HAVE enough invested money to still live comfortably on half, but in 10 years my wife and I will also be taking Social Security at that time to the tune of a little more than $50,000 a year (even more if we wait until after age 62 which we probably won't do), PLUS, I currently have about 3.5 years of expenses saved liquid, so even if the market lost 99% of its value in 10 years, I would just suspend taking from that pile and use Social Security and my liquid savings to live on until the market rebounded (because it would).

Flagpole ,,- if you say the market won't fall 50% in the next 10 years - we believe you! No one else in the world has beaten the Dow 35 out of the last 32 years!

No need to believe me. What event would you expect to happen that would cause a 50% drop in the market?

Percentages aside, what you do to insulate yourself against a DOWN market is you get rid of debt including owning your home outright, and you consistently put at least 15% or your income into stock-containing mutual funds. If you greatly decrease your outgo, espeically in retirement, you can easily handle a down market. Extra cash on the side is good too.

Also, "all that work?" What work? I have money in mutual funds. No work at all on my part. That's actually part of my philosophy. Keep money in mutual funds so that I don't HAVE to do any work. Methinks you didn't know enough about me to comment.

Flagpole’s modus operandi of “follow along with what benefits the rich” is as good as any, depending on your position.

It’s good for the rich, but if you aren’t one of them, you won’t weather the storms as will they.

Flag believes himself rich because he and his wife have some public hack income and pensions, and “don’t need” the investments at any particular time. This perspective works as long as things don’t get too bad, which rarely happens.we

1) Most Americans, including you, would consider me rich if you knew my net worth, all attained from early and often investing (though I have inherited a total of $15,000 in my life, so there's that tiny, tiny amount I didn't earn).

2) I am retired. My wife is a college professor and still works.

3) We do not have pensions.

4) Not sure how or why you are so off here, but short of a nuclear war or a Dictator Donald Trump who decides to take the posessions of all Americans, there isn't a situation that would put me in bad straights financially. I have ZERO debt including a paid-for home. I have about 3.5 years of expenses saved LIQUID, at age 62 when my wife and I plan to take Social Security, that will give us north of $50,000 annually, but the biggest thing by far is my investment pile. The amount of money it has earned me in 2024 is unreal, insane. I've earned more in the last 12 months, hell, even the last 6 months, than the vast majority of people even retire with. I have more than enough. The market could drop 90%, and I'd be fine. It WON'T do that, but if it did, it would just be a matter of time before it would rebound, so it's easy to live on SS after age 62 and my cash reserves if I had to for 3-5 years while I wait for the market to recover (because it WOULD).

This turned out correct: A big optimistic 'welcome to 2024' piece in the WSJ saying people are optimistic. SPX up 24% year to date so far.

Wall Street is feeling sunny about the stock market as the calendar flips to 2024. Last year’s widespread skepticism proved to be misplaced. Stocks rose through much of 2023, powered by the rise of artificial intelligence and an economy that stayed stronger than nearly all of Wall Street had anticipated. The recession that investors had largely agreed was imminent never came. Now, with the S&P 500 within 0.6% of a record high, the crowd is much more optimistic. Behind the dramatic turn in attitude is a growing belief among investors that the Federal Reserve’s campaign to fight inflation is winding down, ending the interest-rate hikes that buffeted markets in recent years. Many now expect the central bank will likely next cut rates instead, shifting market dynamics in ways that seemed unlikely just months ago.

Another good prediction here from a year ago...Zandi said inflation would be back to around 2% by now. It's in the 2-3% zone, so I'll give him the win .

Mark Zandi @Markzandi As a professional economist, I do lots of forecasting. Some forecasts I’m confident in, some not so much. I’m confident that the growth in consumer prices for shelter is headed much lower and that this will push overall inflation back near the Fed’s target by this time next year.

Flagpole’s modus operandi of “follow along with what benefits the rich” is as good as any, depending on your position.

It’s good for the rich, but if you aren’t one of them, you won’t weather the storms as will they.

Flag believes himself rich because he and his wife have some public hack income and pensions, and “don’t need” the investments at any particular time. This perspective works as long as things don’t get too bad, which rarely happens.we

1) Most Americans, including you, would consider me rich if you knew my net worth, all attained from early and often investing (though I have inherited a total of $15,000 in my life, so there's that tiny, tiny amount I didn't earn).

2) I am retired. My wife is a college professor and still works.

3) We do not have pensions.

4) Not sure how or why you are so off here, but short of a nuclear war or a Dictator Donald Trump who decides to take the posessions of all Americans, there isn't a situation that would put me in bad straights financially. I have ZERO debt including a paid-for home. I have about 3.5 years of expenses saved LIQUID, at age 62 when my wife and I plan to take Social Security, that will give us north of $50,000 annually, but the biggest thing by far is my investment pile. The amount of money it has earned me in 2024 is unreal, insane. I've earned more in the last 12 months, hell, even the last 6 months, than the vast majority of people even retire with. I have more than enough. The market could drop 90%, and I'd be fine. It WON'T do that, but if it did, it would just be a matter of time before it would rebound, so it's easy to live on SS after age 62 and my cash reserves if I had to for 3-5 years while I wait for the market to recover (because it WOULD).

Curious how much folks expect to spend in retirement, which is an important factor. Personally, we have fairly ambitious lifestyle spending plans for the early years of retirement (next 15 to 20 years, say). Of course we COULD cut back our spending to basic lifestyle expenses, which would be covered by pensions, but that would sort of defeat the purpose of the hard work we did to earn and save while working.

Ok but a year ago economists thought there was a 100% chance of a recession. 100%. No chance of being wrong. And that was a short term prediction. Now here's GS trying to predict 10 years of equity and bond returns. Absurd.

modest proposal @modestproposal1 · 6h Goldman strategists calculate a 72% probability that 10 year treasuries outperform the S&P 500 over the next decade

this poster took a look at GS's 10 year forecasts in 2012 and 2020 and found them both looking too pessimistic.

Goldman published 10-year forecasts in 2012 and 2020. The 2012 forecast was way too conservative. The 2020 forecast is proving too conservative... https://t.co/IoMXD0p3aGpic.twitter.com/3Jbld87ZNi

1) Most Americans, including you, would consider me rich if you knew my net worth, all attained from early and often investing (though I have inherited a total of $15,000 in my life, so there's that tiny, tiny amount I didn't earn).

2) I am retired. My wife is a college professor and still works.

3) We do not have pensions.

4) Not sure how or why you are so off here, but short of a nuclear war or a Dictator Donald Trump who decides to take the posessions of all Americans, there isn't a situation that would put me in bad straights financially. I have ZERO debt including a paid-for home. I have about 3.5 years of expenses saved LIQUID, at age 62 when my wife and I plan to take Social Security, that will give us north of $50,000 annually, but the biggest thing by far is my investment pile. The amount of money it has earned me in 2024 is unreal, insane. I've earned more in the last 12 months, hell, even the last 6 months, than the vast majority of people even retire with. I have more than enough. The market could drop 90%, and I'd be fine. It WON'T do that, but if it did, it would just be a matter of time before it would rebound, so it's easy to live on SS after age 62 and my cash reserves if I had to for 3-5 years while I wait for the market to recover (because it WOULD).

Curious how much folks expect to spend in retirement, which is an important factor. Personally, we have fairly ambitious lifestyle spending plans for the early years of retirement (next 15 to 20 years, say). Of course we COULD cut back our spending to basic lifestyle expenses, which would be covered by pensions, but that would sort of defeat the purpose of the hard work we did to earn and save while working.

I, personally, don't have an amount I plan to spend. I have mostly inexpensive interests...I fish A LOT. I play my guitars and keyboards A LOT (that CAN be expensive, but I already own what I want and don't plan any outrageous new purchases...I may buy some new gear, but it will be chump change in the grand scheme of things), I work out, I play games online, I watch stuff on the 6 streaming services I have, I take my dog to the dog park. Really, the only extravagant expense I would like to have is I'd like a house with a bowling alley (2 lanes) in it. We'll see. Gotta have the right property to be able to install one if not already there, and since I don't want a mansion, It's unlikely I could find a house the size I want that already has one.

The guidance from retirement planners is to plan for:

The Go Go years: These are the years you want to travel, fulfill bucket lists, etc. These are years when you are still young enough to do such things.

The Slow Go years: You're getting older and so you don't travel as much, and you are beginning to take it easy.

The No Go years: You are in the last years of your life, and you don't spend much time if ANY time traveling. These CAN be expensive years if you need long-term care, but purchasing Long Term Care insurance beginning at age 60 should help with that.

1) Most Americans, including you, would consider me rich if you knew my net worth, all attained from early and often investing (though I have inherited a total of $15,000 in my life, so there's that tiny, tiny amount I didn't earn).

2) I am retired. My wife is a college professor and still works.

3) We do not have pensions.

4) Not sure how or why you are so off here, but short of a nuclear war or a Dictator Donald Trump who decides to take the posessions of all Americans, there isn't a situation that would put me in bad straights financially. I have ZERO debt including a paid-for home. I have about 3.5 years of expenses saved LIQUID, at age 62 when my wife and I plan to take Social Security, that will give us north of $50,000 annually, but the biggest thing by far is my investment pile. The amount of money it has earned me in 2024 is unreal, insane. I've earned more in the last 12 months, hell, even the last 6 months, than the vast majority of people even retire with. I have more than enough. The market could drop 90%, and I'd be fine. It WON'T do that, but if it did, it would just be a matter of time before it would rebound, so it's easy to live on SS after age 62 and my cash reserves if I had to for 3-5 years while I wait for the market to recover (because it WOULD).

Might want to reconsider taking Social Security at 62, locking in a much smaller SS check each year for rest of your life. Unless there are health issues, and you don't plan on living too long. Instead you could draw same amount out of your IRA bucket yearly which allows you SS payment to grow 8% each and every year up until you reach 70. This method also reduces a little you IRA balance to reduce the size of your RMD's at age 73ish.

1) Most Americans, including you, would consider me rich if you knew my net worth, all attained from early and often investing (though I have inherited a total of $15,000 in my life, so there's that tiny, tiny amount I didn't earn).

2) I am retired. My wife is a college professor and still works.

3) We do not have pensions.

4) Not sure how or why you are so off here, but short of a nuclear war or a Dictator Donald Trump who decides to take the posessions of all Americans, there isn't a situation that would put me in bad straights financially. I have ZERO debt including a paid-for home. I have about 3.5 years of expenses saved LIQUID, at age 62 when my wife and I plan to take Social Security, that will give us north of $50,000 annually, but the biggest thing by far is my investment pile. The amount of money it has earned me in 2024 is unreal, insane. I've earned more in the last 12 months, hell, even the last 6 months, than the vast majority of people even retire with. I have more than enough. The market could drop 90%, and I'd be fine. It WON'T do that, but if it did, it would just be a matter of time before it would rebound, so it's easy to live on SS after age 62 and my cash reserves if I had to for 3-5 years while I wait for the market to recover (because it WOULD).

Might want to reconsider taking Social Security at 62, locking in a much smaller SS check each year for rest of your life. Unless there are health issues, and you don't plan on living too long. Instead you could draw same amount out of your IRA bucket yearly which allows you SS payment to grow 8% each and every year up until you reach 70. This method also reduces a little you IRA balance to reduce the size of your RMD's at age 73ish.

I think that is generally good advice. The breakeven point for FRA (Full Retirement Age) versus waiting is about age 82. Unfortunately health issues can pop up unexpectedly, like my cancer at a seemingly healthy age 67.

its an interesting problem. why housing is so expensive.

both parties seem willing to reduce red tape to make building housing cheaper so that will help eventually.

but we have a no-growth aging population or a very low growth population..why exactly will we need more housing? Maybe fewer marriages, more solo living?

Seems to me at some level the market is saying 'it's not profitable for us to build housing so we won't do it.'

Question is why is the market failing. Is it just an over regulated marketplace or something else, like homebuilders smelling a shrinking population that does not really need more housing.

Maybe it's just a long memory of the housing crisis...homebuilders simply do not want to risk anything like that ever again. Still fighting the last war and not building more than they absolutely know they can sell.

This post was edited 1 minute after it was posted.

“Things develop over time. I personally see nothing wrong with the "quality" of immigrants flooding over the border, even if their educational qualifications are zero, or faked--as long as that fraud doesn't carry over to what they do while here.”

Well, when you allow the breaking of immigration laws, and then illegally pay them subsistence to live in this Country, you are subsidizing fraud. I haven’t even touched the illegal voting issue.

As I am a licensed attorney, also before the federal government, I am all about the rule of law. I do not endorse, condone, or support unlawful activity, including any and all violations of immigration laws.

In the real world, nobody is perfect. Heck even priests go to confession! The point is that society has decided what sanctions are to be levied for unlawful behavior, against whom, and when. I'm not talking about just judges, I'm talking about the whole system, including limited funding, selective enforcement, etc. In totality the US, as a society through its elected representatives and institutions, has decided to treat illegal immigration in a particular fashion.

I understand that you don't support that social decision, and neither do many others. I personally don't support some of the ways in which immigration policy is being articulated and implemented, especially as a lawful immigrant myself.

However, when the shtf in one's life, one does what one must--including potentially violating some laws somewhere. Ask your daughter about the doctrine of efficient breach.

If any sanction is imposed, and if it is paid in a timely fashion, there is no administrative ground for complaint. Yes the system is currently overwhelmed and not working as intended, and that raises a host of issues--however, I don't necessarily fault the individuals for their actions, I fault the government for its.

There is still time to "make it work". Yes costs like support are borne now, which is part of the reason we deficit spend. It might be considered a capital outlay. What is the NPV of the future wealth generation by an immigrant and his/her progeny?

There are many factors to consider. Don't worry Igy, YOU are likely not the one who will pay the price! It is deficit spending that later generations may pay, including maybe myself...although I'm no longer a spring chicken either!

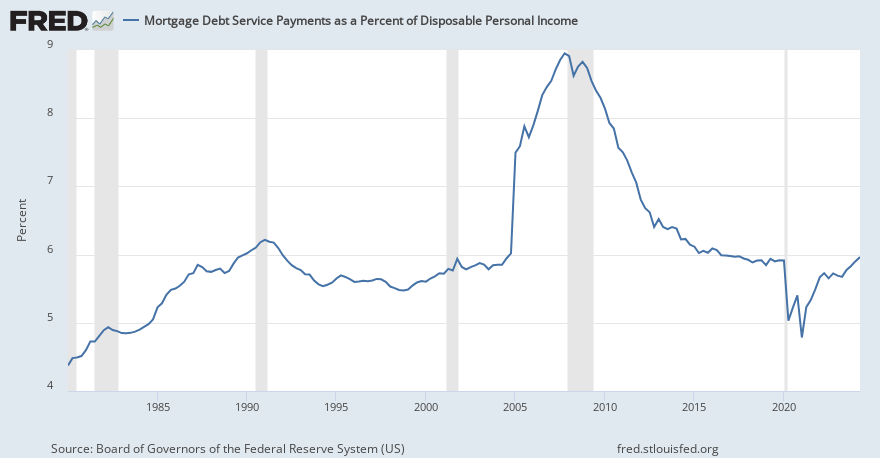

On that train of thought, the debt service payments are becoming a real issue. I hear they just passed military spending. If the US is to succeed in this, it needs to be careful, and I don't trust the social engineers because I know a few of them.

Very few things are black-and-white. I STILL encourage everyone to have a viable Plan B, and maybe C. They help me sleep at night, albeit on a hair trigger.

the problem with stats like this saying 'housing is unaffordable' is that incomes have gone up so much, mortgage payments as a percent of disposable income...are the same as they always were. Suggesting housing is not so hard to afford. Complicated by the huge number of people with no mortgage at all though.

And yet you seem pretty certain of the coming effects of the upcoming election on markets? Maybe you think you CAN have your cake and eat it too…

It was a long time ago that I gave up pointing out things like that. Remember that this is just a message board, that posts aren't necessarily much considered, and that this applies to all of us.

It has its own value if you know how to interpret it.