-

00

-

Sally Vix wrote:

apparently he made $39 million last year. Mostly stock- salary around a million.

00 -

I think we can firmly take 'recession is imminent' talk off the table.

New NowCast for GDP in the 2Q is a red-hot 3.9%.

No, that doesn't help stocks or bonds, probably. Because rates will keep climbing on that. Although the Fed does think inflation is still falling and just 3-4%. So not too bad, that.

Latest estimate: 3.9 percent -- August 01, 2023

10 -

Stater of the obvious wrote:

Ghost of Igloi wrote:

Flagpole or anyone else can refer to my comments as predictions if they like. I did not push back hard on his perma-bear comment any more than this is a hard push back. My comments generally are directed toward valuation of the market, which historically has been a reliable predictor of long term returns. The historical GAAP multiple of the S&P 500 is around 16. Flagpole and others talk often about historical returns in the market, but ignore or discount valuation; the math of price of the market divided by GAAP EPS of the market. In this case, the S&P 500 being a proxy for the market.

Igy, I think the overwhelming majority of intelligent readers here realize that your posts are the work of a consummate troll. Well done, sir.

02 -

Ghost of Igloi wrote:

Sally Vix wrote:

You're talking Flagpole money now. I am sure he will be predicting that stocks will tank in 2024, just like Hussman.

Speaking of the later:

01 -

From a year ago.

⚠️ Latest Zoltan

💰 Pozsar Says L-Shaped Recession Is Needed to Conquer Inflation

🔹 Fed may have to hike to 5% or 6% as inflation now structural

🔹 Economic war has broken out and wars are inflationary: PoszarThis guy was an economist at Credit Suisse. Which raises questions about his judgment, right? Remember what happened to them? Anyway, interesting that he was right that the Fed would hike to 5-6% but he seems to have thought that would cause a recession. When in fact rates ARE now at 5-6% but the economy is accelerating.

And inflation has cratered even without the recession.

Strange times.

10 -

Remember last year people would draw the 2022 market onto 1974, 1987, 2000, 2008? Suggesting that we were about to get a market crash like in those years? Yeah nah. Didn't work out.

10 -

agip wrote:

Remember last year people would draw the 2022 market onto 1974, 1987, 2000, 2008? Suggesting that we were about to get a market crash like in those years? Yeah nah. Didn't work out.

Adding another $Trillion to the National credit card goes a long way. The negative affect of that is priced into a whole host of assets, just not the Fav Seven. At least not yet.

This post was edited 3 minutes after it was posted.01 -

Ghost of Igloi wrote:

agip wrote:

Remember last year people would draw the 2022 market onto 1974, 1987, 2000, 2008? Suggesting that we were about to get a market crash like in those years? Yeah nah. Didn't work out.

Adding another $Trillion to the National credit card goes a long way. The negative affect of that is priced into a whole host of assets, just not the Fav Seven. At least not yet.

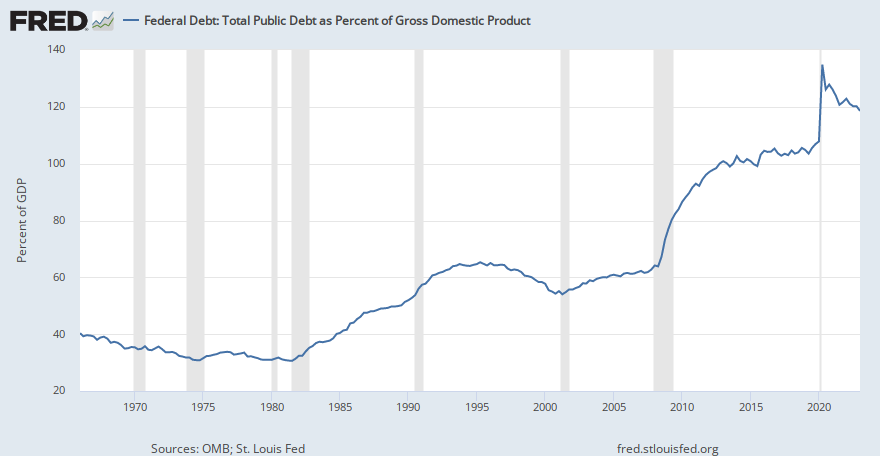

debt/GDP has fallen a lot over the last three years so have to be careful on this.

10 -

Stater of the obvious wrote:

Ghost of Igloi wrote:

Flagpole or anyone else can refer to my comments as predictions if they like. I did not push back hard on his perma-bear comment any more than this is a hard push back. My comments generally are directed toward valuation of the market, which historically has been a reliable predictor of long term returns. The historical GAAP multiple of the S&P 500 is around 16. Flagpole and others talk often about historical returns in the market, but ignore or discount valuation; the math of price of the market divided by GAAP EPS of the market. In this case, the S&P 500 being a proxy for the market.

Igy, I think the overwhelming majority of intelligent readers here realize that your posts are the work of a consummate troll. Well done, sir.

Nope! His posts are those of a permabear, and by definition he will be wrong on an annual basis about 73% of the time.

Also, there is no "taking" his comments as a prediction. In the comment of his that I will monitor through the end of this calendar year, he said that the S&P 500 will end up at or around 3000, and he said so when it stood at 3991 (it's now around 4500). I called him a permabear (which he is), and then he asked agip to bookmark the page, thus showing how confident he was in this short term prediction.

From 2/23/2023:

Ghost of Igloi wrote: The period of S&P 500 companies over earning has ended. Stimulus, low interest rates done, higher labor costs, margins shrinking. Last year 2022 GAAP EPS down to $171. I expect by Q3 2023 the previous 52 week number to be in the $150s. Hard to see a year end 2023 S&P 500 much above 3,000, even without a recession.

Flagpole wrote: Permabear.

Ghost of Igloi wrote: Agip, if you don’t mind bookmark this for year end review.

20 -

Flagpole wrote:

Stater of the obvious wrote:

Igy, I think the overwhelming majority of intelligent readers here realize that your posts are the work of a consummate troll. Well done, sir.

Nope! His posts are those of a permabear, and by definition he will be wrong on an annual basis about 73% of the time.

Also, there is no "taking" his comments as a prediction. In the comment of his that I will monitor through the end of this calendar year, he said that the S&P 500 will end up at or around 3000, and he said so when it stood at 3991 (it's now around 4500). I called him a permabear (which he is), and then he asked agip to bookmark the page, thus showing how confident he was in this short term prediction.

From 2/23/2023:

Ghost of Igloi wrote: The period of S&P 500 companies over earning has ended. Stimulus, low interest rates done, higher labor costs, margins shrinking. Last year 2022 GAAP EPS down to $171. I expect by Q3 2023 the previous 52 week number to be in the $150s. Hard to see a year end 2023 S&P 500 much above 3,000, even without a recession.

Flagpole wrote: Permabear.

Ghost of Igloi wrote: Agip, if you don’t mind bookmark this for year end review.

Yes, he is wrong most of the time. So either he is a troll, or a complete idiot. I mean, it’s hard to be wrong that often, isn’t it? One look at the moronic tweets he posts suggests trolling to me. Anyway, his posts are good for a chuckle and not much more. It seems most here just ignore him.

10 -

10 year up to 4.18%, near the cyclical high.

sounds like the market is now saying the Fed will blink and let inflation stay at 3-4%, and the bond vigilantes are therefore requiring higher rates to compensate for a higher inflation rate.

inter and long term bonds getting crushed again.

20 -

Flagpole wrote:

Stater of the obvious wrote:

Igy, I think the overwhelming majority of intelligent readers here realize that your posts are the work of a consummate troll. Well done, sir.

Nope! His posts are those of a permabear, and by definition he will be wrong on an annual basis about 73% of the time.

Also, there is no "taking" his comments as a prediction. In the comment of his that I will monitor through the end of this calendar year, he said that the S&P 500 will end up at or around 3000, and he said so when it stood at 3991 (it's now around 4500). I called him a permabear (which he is), and then he asked agip to bookmark the page, thus showing how confident he was in this short term prediction.

From 2/23/2023:

Ghost of Igloi wrote: The period of S&P 500 companies over earning has ended. Stimulus, low interest rates done, higher labor costs, margins shrinking. Last year 2022 GAAP EPS down to $171. I expect by Q3 2023 the previous 52 week number to be in the $150s. Hard to see a year end 2023 S&P 500 much above 3,000, even without a recession.

Flagpole wrote: Permabear.

Ghost of Igloi wrote: Agip, if you don’t mind bookmark this for year end review.

Can Igy still edit that post so he doesn't look so silly on 12/31/23?

10 -

01

-

Stater of the obvious wrote:

Flagpole wrote:

Nope! His posts are those of a permabear, and by definition he will be wrong on an annual basis about 73% of the time.

Also, there is no "taking" his comments as a prediction. In the comment of his that I will monitor through the end of this calendar year, he said that the S&P 500 will end up at or around 3000, and he said so when it stood at 3991 (it's now around 4500). I called him a permabear (which he is), and then he asked agip to bookmark the page, thus showing how confident he was in this short term prediction.

From 2/23/2023:

Ghost of Igloi wrote: The period of S&P 500 companies over earning has ended. Stimulus, low interest rates done, higher labor costs, margins shrinking. Last year 2022 GAAP EPS down to $171. I expect by Q3 2023 the previous 52 week number to be in the $150s. Hard to see a year end 2023 S&P 500 much above 3,000, even without a recession.

Flagpole wrote: Permabear.

Ghost of Igloi wrote: Agip, if you don’t mind bookmark this for year end review.

Yes, he is wrong most of the time. So either he is a troll, or a complete idiot. I mean, it’s hard to be wrong that often, isn’t it? One look at the moronic tweets he posts suggests trolling to me. Anyway, his posts are good for a chuckle and not much more. It seems most here just ignore him.

I won't go so far as to call him an idiot (he's right up knocking on the door though), but he's completely wrong about how he views the markets. He tries to inject some intellectual nonsense in there where none belongs. He tries to time things. Men seem to get some sort of macho attachment to the stock market, and it's really silly. Investing in the stock market isn't intellectual. It isn't macho. It is VERY simple, and the most important thing to do regarding the stock market is to just DO IT. Invest. Do it ALL the time. Never stop. Don't worry about peaks and valleys, and just invest, invest, invest as much of your income as you can until you are ready to retire. Mutual funds made up of stocks as the vast majority of your holdings.

30 -

Changing my name a bit over time as we transition away from work into retirement. Coming up on most of a year now, and things seem to be working out OK (for us), so I think I'll carry on with this name after transitioning from various forms of "idiot" (speaking of idiots) to nearly retired, then newly retired and most recently, retiree, which felt clumsy.

Question for Flagpole, or others, about mutual funds. I haven't bought one deliberately in maybe 25 years, since transitioning to individual stocks (in diversified baskets), then (mostly) ETFs, some bonds, and, most recently, various forms of "cash." Are there decent mutual funds out there with low MERs? That's frankly what drove me away so long ago and I've never looked back. Thoughts / comments? Would be keen to know if any on here see some particular advantage in buying mutual funds versus ETFs.

10 -

comfortably retired wrote:

Changing my name a bit over time as we transition away from work into retirement. Coming up on most of a year now, and things seem to be working out OK (for us), so I think I'll carry on with this name after transitioning from various forms of "idiot" (speaking of idiots) to nearly retired, then newly retired and most recently, retiree, which felt clumsy.

Question for Flagpole, or others, about mutual funds. I haven't bought one deliberately in maybe 25 years, since transitioning to individual stocks (in diversified baskets), then (mostly) ETFs, some bonds, and, most recently, various forms of "cash." Are there decent mutual funds out there with low MERs? That's frankly what drove me away so long ago and I've never looked back. Thoughts / comments? Would be keen to know if any on here see some particular advantage in buying mutual funds versus ETFs.

I'm not one to advise you on specific funds. I just do not think of investing in that way. Funds can do well one year and then not so well the next. Diversify (seems like you are, and I especially like how you have invested in individual stocks (diversified baskets) as that's the only way it should be done). As you are retired, unless an ailment forced you there, I can only assume that you were happy enough with your financial life to be able to do so. If that's the case and you are pleased with the income your investments bring you, then there's probably no need to make any changes.

10 -

comfortably retired wrote:

Changing my name a bit over time as we transition away from work into retirement. Coming up on most of a year now, and things seem to be working out OK (for us), so I think I'll carry on with this name after transitioning from various forms of "idiot" (speaking of idiots) to nearly retired, then newly retired and most recently, retiree, which felt clumsy.

Question for Flagpole, or others, about mutual funds. I haven't bought one deliberately in maybe 25 years, since transitioning to individual stocks (in diversified baskets), then (mostly) ETFs, some bonds, and, most recently, various forms of "cash." Are there decent mutual funds out there with low MERs? That's frankly what drove me away so long ago and I've never looked back. Thoughts / comments? Would be keen to know if any on here see some particular advantage in buying mutual funds versus ETFs.

an index fund following, say, big cap US stocks will be almost exactly the same whether it is an ETF or traditional mutual fund. There are some difference in taxation and behavioral investing, but that's in the weeds a bit. A Schwab SP500 ETF will have virtually the same results and characteristics as a Vanguard Sp500 mutual fund.

But once you get into actively managed traditional mutual funds there are many differences between ETFs and traditional mutual funds.

10