Interest rates are too high right now. Continue to save money and stash it away in the house fund. When Trump becomes President in 2025, the economy will get better and inflation/interest rates will go back to normal.

Do you have any non-retirement savings? If you don't live an extravagant life, don't be afraid to stretch the normal bounds. The rule I heard when buying a decade ago was to not buy above about 4X your annual gross salary. I probably went closer to 5X. A little "house poor" at times in the early years of ownership, but no regrets. And I make a lot more than when I bought the home now, so feels cheap (particularly with a fixed 2.x% mortgage).

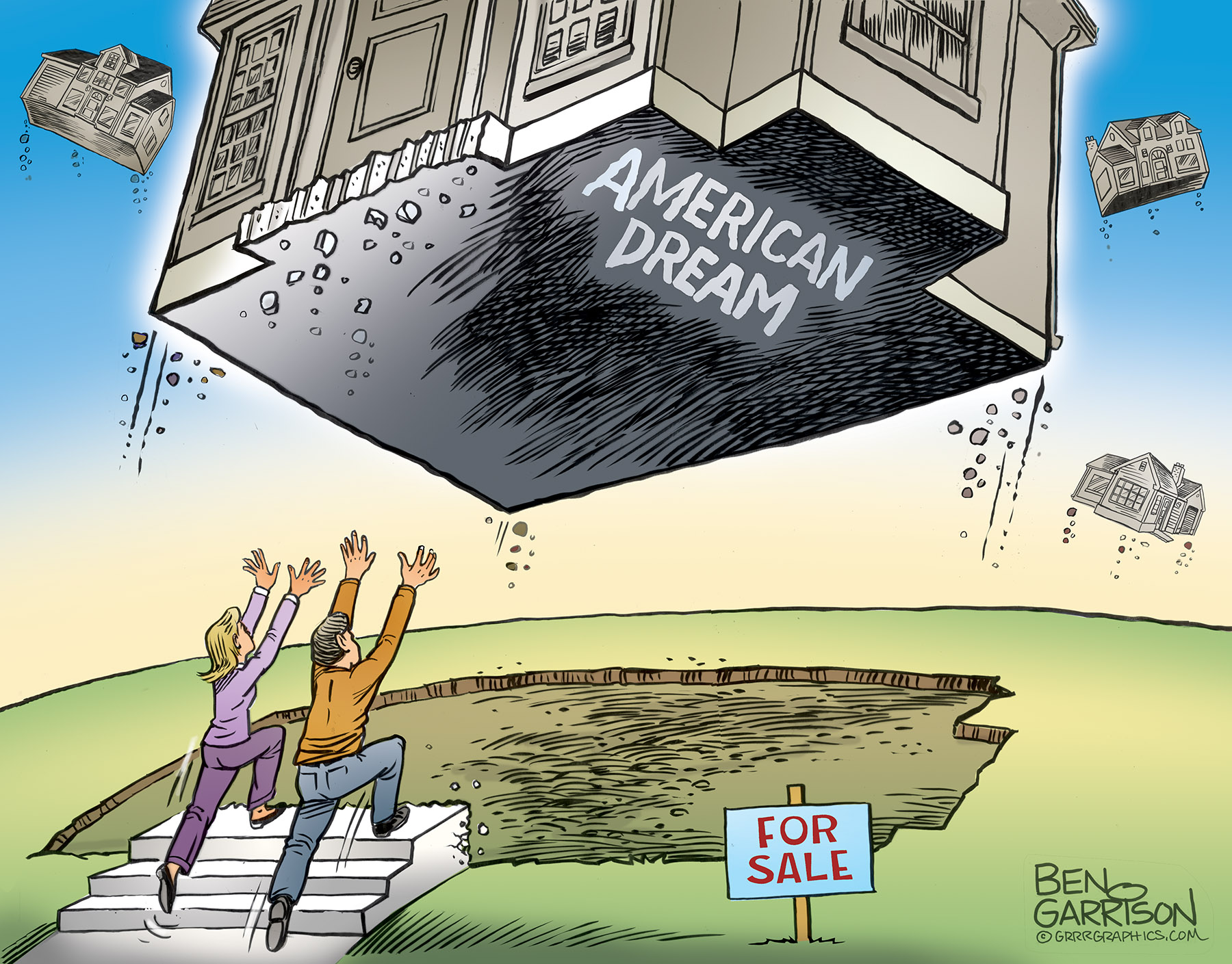

I am 28 and make 80k a year. After taxes and elective contribution, I get $1,950 a paycheck every 2 weeks. So for 10 of 12 months, that means $3,900 in take home pay. Based on boomer-era finanical advice, 28% should be spent on a mortgage. That's $1,092 MAXIMUM. Reverse-engineer that, and even with a full 20% down, that's around a $170k house.

I live in a town of 25k in the midwest. There are 67 houses for sale. 2 are technically in my budget. One is completely torn up for a full reno on the inside. The other is 800 sq ft foreclosure with no garage door.

If you are older than me, and you EVER wonder why so many people my age and younger are "antiwork", or "soy leftists", or rent their childhood bedroom from their parents (like me), or don't go to college, or whatever f***ing problem you have with them, THIS IS WHY. The math is impossible. It's not going to get better. Somehow, it's going to get mathematically more difficult to afford a house, every year, forever, and no one is ever going to step in and fix it on a state, national, political, or investment level.

The 28% is on your GROSS MONTHLY PAY. That is $80,000/12 = $6,666.66 * 0.28 = $1,866.67. On a 30 year at 7%, that is $280,000 loan. If you factor in taxes and insurance, you probably shouldn't borrow more than about $260,000. If you have a 20% down payment (65k). That puts you at a home for $325,000. So you can afford house.

I am 28 and make 80k a year. After taxes and elective contribution, I get $1,950 a paycheck every 2 weeks. So for 10 of 12 months, that means $3,900 in take home pay. Based on boomer-era finanical advice, 28% should be spent on a mortgage. That's $1,092 MAXIMUM. Reverse-engineer that, and even with a full 20% down, that's around a $170k house.

I live in a town of 25k in the midwest. There are 67 houses for sale. 2 are technically in my budget. One is completely torn up for a full reno on the inside. The other is 800 sq ft foreclosure with no garage door.

If you are older than me, and you EVER wonder why so many people my age and younger are "antiwork", or "soy leftists", or rent their childhood bedroom from their parents (like me), or don't go to college, or whatever f***ing problem you have with them, THIS IS WHY. The math is impossible. It's not going to get better. Somehow, it's going to get mathematically more difficult to afford a house, every year, forever, and no one is ever going to step in and fix it on a state, national, political, or investment level.

Bad timing. You missed out on sub 3 percent. Hang in there. Also, nothing magic about 28 percent you can stretch to 35 with discipline.

Gen x here. My parents could afford a house on one income. Boomers could also swing that provided they bought early enough.

We could swing it on two incomes however I could not buy a house where I was raised.

Now it is out of reach unless you inherit a house or both you and your partner are making bank.

I have actually had the same thoughts as you. Why work so hard if there is little hope of having something that belongs to you?

I am not sure what the answer is but my kids are both in their early twenties and I don’t see any relief in sight for them. You want to see your kids have a better life than you. That was always part of the dream for me. We can’t help them much because we are getting wrecked by taxes.

Rent cheaply and save money for a large down payment. Or get married. Or just be like any other normal single dude

A lot of single guys I know even in their 40s rent and plan to do so for a while--they put their income into savings or spend it on fun things in life.

For the first time, three-time Olympic athlete Suzy Favor Hamilton is revealing what fueled her double life as a celebrated track hero and a Vegas escort.

Purchased my first home in 2013 - $195,000 on a $42,000 salary

Sold in 2018 ($305,000) - rented for the next 6 months.

Purchased second home in 2019 - $252,000 on a $49,000 salary

Sold that home last month ($386,000)

Purchased third home this month ($365,000) on a $56,000 salary

I'm a teacher, so I don't make a ton. My wife has a small business that brings in about another $15-20K annually.

The investment of the home has to make sense for you. We knew the first two homes were ones we would live in for 3-5 years and renovate to turn a profit. Now we have what we would consider a dream property, but it has been ten years in the making. Could have gotten there quicker with higher income, but we made due with what we had.

I will say that we never considered any kind of % of income as a benchmark for mortgage payments. We looked at the whole situation more as a total financial package + quality of life and made decisions based on that.

Gen x here. My parents could afford a house on one income. Boomers could also swing that provided they bought early enough.

We could swing it on two incomes however I could not buy a house where I was raised.

Now it is out of reach unless you inherit a house or both you and your partner are making bank.

I have actually had the same thoughts as you. Why work so hard if there is little hope of having something that belongs to you?

I am not sure what the answer is but my kids are both in their early twenties and I don’t see any relief in sight for them. You want to see your kids have a better life than you. That was always part of the dream for me. We can’t help them much because we are getting wrecked by taxes.

Good post.

I think there is no shame in renting--keep the lights on, the roof over our heads and just survive.

My wife makes 47 and I am finally at 60k at age 39. Very grateful. So much better than the 38k I was at before at age 38. But even still, it's going to be rent city for a few years. Luckily we live in a modest, but solid, apartment.

You're only 28. Second 80K is not much these days even in midwest. Maybe before Covid but now with inflation, everything is out of whack. You need to earn at least 30K more to make up for what happened in last 4 years. Save up for another year or two and put up more down payment.

Condescending advice that was never given to generations of homebuyers in this country. Avoiding talking about the real problem entirely and shifting blame entirely onto individuals instead of the f*cked market.

Maybe you should go into housebuilding or creative financing to provide something more affordable. Or maybe you could buy and rent a portion of your house to a worthy housemate. Or ....

But Republicans refuse policies like pension, universal healthcare, free higher education that will ease the burden on working folks. All they care about is tax cuts for millionaires and billionaires.

Laws should be made that outlaw corporate ownership of homes and flipping of homes since they both seriously drive up inflation without contributing the the general welfare of the nation. Homes are meant for families.

The 28% is on your GROSS MONTHLY PAY. That is $80,000/12 = $6,666.66 * 0.28 = $1,866.67. On a 30 year at 7%, that is $280,000 loan. If you factor in taxes and insurance, you probably shouldn't borrow more than about $260,000. If you have a 20% down payment (65k). That puts you at a home for $325,000. So you can afford house.

OP can't afford a house because he is terrible at maths. Even if he did buy a house, he'd still be on here bitching about property taxes and maintenance costs 🤡

Help us build the best running shoe review site for a chance to win a LetsRun t-shirt.Help us build the best running shoe review site for a chance to win one of 10 LetsRun t-shirts.