Flagpole - don't take this the wrong way but not sure you understand the markets too well. The Flagpole YTD of 11% - is that capital appreciation or also including dividends? Same with the markets. Only cap. Appreciation or also dividends. This might be 2 bad years for you. I have a ranch with bunkhouse you and your lovely wife can stay in. No charge!

1) Um...there is nothing about what I have provided there that I don't understand.

2) I'll leave the "including dividends" to myself just to bother you.

3) Might be a bad 2 years for me? Ha! What are you talking about? I'm not just barely above water, brother. I've won the financial battle. I have more money than I will ever need even if the market goes down every year from here until I die (and it won't). This is why you don't ever see me fretting about the direction of the market or crowing that I sold X and made this or that on a short-term sale. I don't care. I don't need to care. I've put myself in a position to not have to care due to consistent, unwavering HUGE investing since 1989.

4) Hard truth...I would rather stick a Tabasco-soaked finger in my eye than spend even one minute under the same room with you. I have no place in my life for Trumpers.

Bit harsh but we three - me, you and the lovely Ms Flagpole - would rock together. Does she like breakfast in bed?

1) Um...there is nothing about what I have provided there that I don't understand.

2) I'll leave the "including dividends" to myself just to bother you.

3) Might be a bad 2 years for me? Ha! What are you talking about? I'm not just barely above water, brother. I've won the financial battle. I have more money than I will ever need even if the market goes down every year from here until I die (and it won't). This is why you don't ever see me fretting about the direction of the market or crowing that I sold X and made this or that on a short-term sale. I don't care. I don't need to care. I've put myself in a position to not have to care due to consistent, unwavering HUGE investing since 1989.

4) Hard truth...I would rather stick a Tabasco-soaked finger in my eye than spend even one minute under the same room with you. I have no place in my life for Trumpers.

Congratulations, FP.

Regarding your comment, Sally, about taking last years declines into the equation when considering this years gains, I did some checking on my own portfolio, and it just so happens that last years downturn exactly equals this years gains ytd thus far in percentage terms.

So, point being, while i don't need to be looking for a ranch bunkhouse, it is instructive to keep these things in perspective in that markets don't only move in only one direction.

The markets definitely don't move in just one direction...they just move in one direction (UP) ~73% of calendar years. Since we know that it is IMPOSSIBLE to predict with any great certainty exactly when the markets will go up and down, the best idea has always been and continues to be to invest a percentage of your income (at least 15%) like clockwork until you retire. Unfortunately people get too emotional with the stock market...they get scared of a big downturn or they attach machismo to investing (and that doesn't belong at all).

Regarding your comment, Sally, about taking last years declines into the equation when considering this years gains, I did some checking on my own portfolio, and it just so happens that last years downturn exactly equals this years gains ytd thus far in percentage terms.

So, point being, while i don't need to be looking for a ranch bunkhouse, it is instructive to keep these things in perspective in that markets don't only move in only one direction.

The markets definitely don't move in just one direction...they just move in one direction (UP) ~73% of calendar years. Since we know that it is IMPOSSIBLE to predict with any great certainty exactly when the markets will go up and down, the best idea has always been and continues to be to invest a percentage of your income (at least 15%) like clockwork until you retire. Unfortunately people get too emotional with the stock market...they get scared of a big downturn or they attach machismo to investing (and that doesn't belong at all).

Fantastic.

Were you so eager last year to post your ytd losses last year even in advance of year end? That eager?

You have one investing style. It seems to fit your temperament and kudos for finding one that suits you. It is not the only style of investing and it is not "the best" as you claim, though it may be the best for your given many things including the time you have to dedicate to it, your risk aversity, the level of your financial assets, other sources of income, years to retirement, etc., to name just a few.

The markets definitely don't move in just one direction...they just move in one direction (UP) ~73% of calendar years. Since we know that it is IMPOSSIBLE to predict with any great certainty exactly when the markets will go up and down, the best idea has always been and continues to be to invest a percentage of your income (at least 15%) like clockwork until you retire. Unfortunately people get too emotional with the stock market...they get scared of a big downturn or they attach machismo to investing (and that doesn't belong at all).

Fantastic.

Were you so eager last year to post your ytd losses last year even in advance of year end? That eager?

You have one investing style. It seems to fit your temperament and kudos for finding one that suits you. It is not the only style of investing and it is not "the best" as you claim, though it may be the best for your given many things including the time you have to dedicate to it, your risk aversity, the level of your financial assets, other sources of income, years to retirement, etc., to name just a few.

I'll stop there (but I could go on....)

1) Yes. I DID post several times about my losses last year. Not only did I have a down year last year, but I lost to the Dow also which almost never happens (I will post proof if you challenge me about this). I posted extensively about this. I'm not afraid to discuss down years. I don't just talk about up years. Not how I roll, and that would go against my philosophy of accepting as a given that about 27% of calendar years will be down years.

2) For people who make moderate income from a JOB ($300,000 and less annual family income), not a trust fund or income because you own several apartment buildings or other exceptions which I am always willing to grant if a good case is made, my way of investing is absolutely the right way...the best way. Now, if you want to invest 15% into retirement account mutual funds made up of stocks and NEVER dip below that and then once you are completely debt free including a paid for house, and you have a million dollars minimum invested, you CAN then invest additionally into more risky things like individual stocks or art or antique cars, etc. if you want to. The baseline should always be 15% minimum of your income into retirement account mutual funds though. If you invest as you should from the moment you get a life-supporting job until you retire, you won't need to and likely won't even want to invest in a more risky way...unless you get a thrill out of risk taking which I don't have. If you find that you NEED to invest in a risky way, then you didn't start investing early enough, and you really risk having to work longer than you might have wanted to.

3) My investing strategy deals with risk aversity, nearness to retirement, time in retirement, other sources of income, so that point of yours is moot.

Financial stocks are up 5% from this widely-seen scary tweet.

Markets & Mayhem @Mayhem4Markets Half of US banks have assets worth less than liabilities Almost half of America’s 4,800 banks are already burning through their capital buffers. They may not have to mark all losses to market under US accounting rules but that does not make them solvent. Somebody will take those losses. “It’s spooky. Thousands of banks are underwater,” said Professor Amit Seru, a banking expert at Stanford University. “Let’s not pretend that this is just about Silicon Valley Bank and First Republic. A lot of the US banking system is potentially insolvent.” Source: AP

Good call here (so far) to put aside worries about Apple's China business. Apple up 3% from this tweet, when apple fell sharply. But stock still lower than where it was before the china scare so that's not great.

Carl Quintanilla @carlquintanilla MORGAN STANLEY: “Apple's 2-day -6% stock move suggests the market thinks recent China headlines will evolve into something broader. We believe that's unlikely. .. Reiterate Overweight, $215 target.”[Woodring] $AAPL

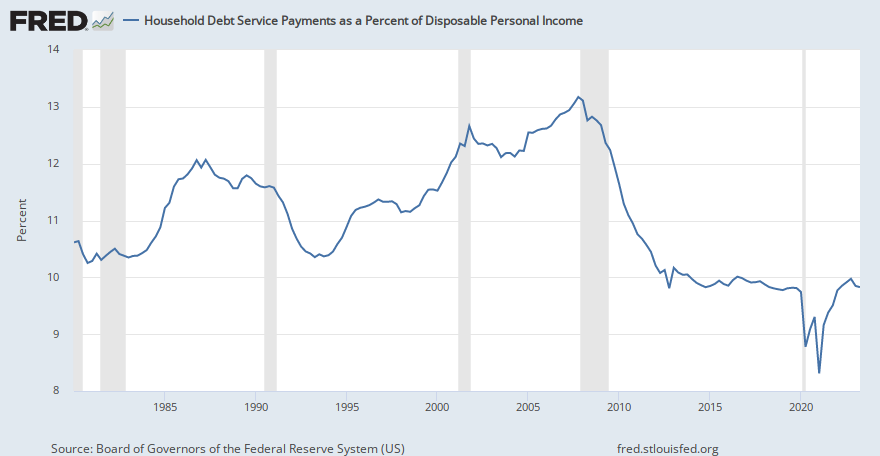

This is always one of my favorite charts. Despite all the worry about consumers and higher interest rates...the household debt service/disposable income ratio is historically low. Shows the rude health of American households.

'Microsoft trades at 30.5 times estimated earnings, below a recent peak of 32.5, but at a sizable premium to its long-term average. 91% of funds own Microsoft, and it is among the most crowded stocks in the sector.' bloomberg.com/news/articles/…

'Microsoft trades at 30.5 times estimated earnings, below a recent peak of 32.5, but at a sizable premium to its long-term average. 91% of funds own Microsoft, and it is among the most crowded stocks in the sector.'

Igy - is there any reason a fund should NOT have MSFT in its portfolio? It is up 400,000% in the last 40 years. Let me say again - up 400,000% in the last 40 years. I am riding that horse until it can't ride anymore.

'Microsoft trades at 30.5 times estimated earnings, below a recent peak of 32.5, but at a sizable premium to its long-term average. 91% of funds own Microsoft, and it is among the most crowded stocks in the sector.'

Igy - is there any reason a fund should NOT have MSFT in its portfolio? It is up 400,000% in the last 40 years. Let me say again - up 400,000% in the last 40 years. I am riding that horse until it can't ride anymore.

Also 8 years ago on page 300 here you were scoffing at those who got TSLA and saying you would get last laugh. TSLA was about $25 back then. Now at $700. Guess you whiffed on that too. Have you ever been right?

Sally, I noticed with the Dow only up 3% this year, you never talk about the index anymore. Remember when you wrote about the marvels of Dow versus CD rates? Boy you would have been much better off in CDs the last 2 1/2 years than the Dow.

Igy - is there any reason a fund should NOT have MSFT in its portfolio? It is up 400,000% in the last 40 years. Let me say again - up 400,000% in the last 40 years. I am riding that horse until it can't ride anymore.

Also 8 years ago on page 300 here you were scoffing at those who got TSLA and saying you would get last laugh. TSLA was about $25 back then. Now at $700. Guess you whiffed on that too. Have you ever been right?

How many shares of TSLA did you savvy wife investor buy 8 years ago?

Also 8 years ago on page 300 here you were scoffing at those who got TSLA and saying you would get last laugh. TSLA was about $25 back then. Now at $700. Guess you whiffed on that too. Have you ever been right?

How many shares of TSLA did you savvy wife investor buy 8 years ago?

Igy you said 8 years that TSLA was junk. You were proved to be extremely wrong. When do you make good predictions? 20 years from now.

Were you so eager last year to post your ytd losses last year even in advance of year end? That eager?

You have one investing style. It seems to fit your temperament and kudos for finding one that suits you. It is not the only style of investing and it is not "the best" as you claim, though it may be the best for your given many things including the time you have to dedicate to it, your risk aversity, the level of your financial assets, other sources of income, years to retirement, etc., to name just a few.

I'll stop there (but I could go on....)

1) Yes. I DID post several times about my losses last year. Not only did I have a down year last year, but I lost to the Dow also which almost never happens (I will post proof if you challenge me about this). I posted extensively about this. I'm not afraid to discuss down years. I don't just talk about up years. Not how I roll, and that would go against my philosophy of accepting as a given that about 27% of calendar years will be down years.

2) For people who make moderate income from a JOB ($300,000 and less annual family income), not a trust fund or income because you own several apartment buildings or other exceptions which I am always willing to grant if a good case is made, my way of investing is absolutely the right way...the best way. Now, if you want to invest 15% into retirement account mutual funds made up of stocks and NEVER dip below that and then once you are completely debt free including a paid for house, and you have a million dollars minimum invested, you CAN then invest additionally into more risky things like individual stocks or art or antique cars, etc. if you want to. The baseline should always be 15% minimum of your income into retirement account mutual funds though. If you invest as you should from the moment you get a life-supporting job until you retire, you won't need to and likely won't even want to invest in a more risky way...unless you get a thrill out of risk taking which I don't have. If you find that you NEED to invest in a risky way, then you didn't start investing early enough, and you really risk having to work longer than you might have wanted to.

3) My investing strategy deals with risk aversity, nearness to retirement, time in retirement, other sources of income, so that point of yours is moot.

Keep up the good work, FP. Regular investing in stock mutual funds by investors like you is exactly what fuels my stock portfolio outperformance.

As they say in that song by Dire Straits (you know the one), 'that's the way you do it!'

You didn’t answer the question, how many shares of TSLA did your savvy investor wife buy 8 years ago?

In regards to TSLA, that company has been largely a government subsidized Green project going back to the GFC.

Igy - you are a fiduciary. Why put your clients portfolios at a loss because you are a Permabear?

Tesla - I said it at the time, getting listed on the SNP 500 index would be it's kiss of death. That was late Dec. 2020, and it trading at the same price today as it was then, almost 3 years later.

1) Yes. I DID post several times about my losses last year. Not only did I have a down year last year, but I lost to the Dow also which almost never happens (I will post proof if you challenge me about this). I posted extensively about this. I'm not afraid to discuss down years. I don't just talk about up years. Not how I roll, and that would go against my philosophy of accepting as a given that about 27% of calendar years will be down years.

2) For people who make moderate income from a JOB ($300,000 and less annual family income), not a trust fund or income because you own several apartment buildings or other exceptions which I am always willing to grant if a good case is made, my way of investing is absolutely the right way...the best way. Now, if you want to invest 15% into retirement account mutual funds made up of stocks and NEVER dip below that and then once you are completely debt free including a paid for house, and you have a million dollars minimum invested, you CAN then invest additionally into more risky things like individual stocks or art or antique cars, etc. if you want to. The baseline should always be 15% minimum of your income into retirement account mutual funds though. If you invest as you should from the moment you get a life-supporting job until you retire, you won't need to and likely won't even want to invest in a more risky way...unless you get a thrill out of risk taking which I don't have. If you find that you NEED to invest in a risky way, then you didn't start investing early enough, and you really risk having to work longer than you might have wanted to.

3) My investing strategy deals with risk aversity, nearness to retirement, time in retirement, other sources of income, so that point of yours is moot.

Keep up the good work, FP. Regular investing in stock mutual funds by investors like you is exactly what fuels my stock portfolio outperformance.

As they say in that song by Dire Straits (you know the one), 'that's the way you do it!'

Ha! Whatever dude. I only care about what my investing does for me. I couldn't care less what you think my investing does for you.

'Microsoft trades at 30.5 times estimated earnings, below a recent peak of 32.5, but at a sizable premium to its long-term average. 91% of funds own Microsoft, and it is among the most crowded stocks in the sector.'

hard question now - do we buy expensive, high-quality stocks like MSFT because that is what has worked for 12+ years? Or do we switch to lower-quality but much cheaper stocks?

No one knows, but certainly buying the expensive stuff has been the ticket for a decade or more.

Help us build the best running shoe review site for a chance to win a LetsRun t-shirt.Help us build the best running shoe review site for a chance to win one of 10 LetsRun t-shirts.