You can look for yourself. His prediction is valuations do not matter, nothing matters, just buy the market. Quite frankly, a rather naive view, yet appropriate for a young investor, with few assets at risk.

Ok, so this tells me that you have no proof and made up what you said. It strikes me as hypocritical that you accuse another poster of lying, then do the same yourself.

1) He said I made a prediction about the S&P 500 which I didn't do. I didn't do it specifically. I didn't imply anything, and I made that crystal clear from the beginning. He won't provide the quote because there isn't one.

2) He says my "prediction" is to just buy the market. Um...that's a philosophy not a prediction...and it IS what people should do. Right from the first job, you need to get rid of small debts as soon as possible (the only large debts that are acceptable to keep before you start investing are a mortgage and a LARGE student loan), and then you put 15% of your income into retirement accounts made up of diversified stock mutual funds. You do that until you retire. You don't stop putting money in. You don't sell. You only buy and buy and buy some more...until you retire. Then, you can stop and take money out.

3) Why do you do this? The market is UNPREDICTABLE. No one on the planet can tell you when it will go up and when it will go down with any level of certainty. So, you go with the FACTS that the market goes up 73% of the time on an annual basis and it always move north over time. If the market when up 100% of the time, then that's where ALL of your efforts should go, but since that's not the case, you need to eliminate debt, secure housing for the rest of your life, and enter retirement with 3 YEARS of expenses liquid...could be in a savings account (even a high yield one), just a checking account earning no interest, or (not my choice) even CDs if you want...as long as you can get at the money if you need to pay bills if the stock market goes down a lot and you don't want to draw from it then.

4) An even better strategy is to invest MORE than the minimum so you can feel confident taking money from your very big pile in retirement even IF the market tanks for several years...BUT most people don't get there.

You can look for yourself. His prediction is valuations do not matter, nothing matters, just buy the market. Quite frankly, a rather naive view, yet appropriate for a young investor, with few assets at risk.

Ok, so this tells me that you have no proof and made up what you said. It strikes me as hypocritical that you accuse another poster of lying, then do the same yourself.

1) He said I made a prediction about the S&P 500 which I didn't do. I didn't do it specifically. I didn't imply anything, and I made that crystal clear from the beginning. He won't provide the quote because there isn't one.

2) He says my "prediction" is to just buy the market. Um...that's a philosophy not a prediction...and it IS what people should do. Right from the first job, you need to get rid of small debts as soon as possible (the only large debts that are acceptable to keep before you start investing are a mortgage and a LARGE student loan), and then you put 15% of your income into retirement accounts made up of diversified stock mutual funds. You do that until you retire. You don't stop putting money in. You don't sell. You only buy and buy and buy some more...until you retire. Then, you can stop and take money out.

3) Why do you do this? The market is UNPREDICTABLE. No one on the planet can tell you when it will go up and when it will go down with any level of certainty. So, you go with the FACTS that the market goes up 73% of the time on an annual basis and it always move north over time. If the market when up 100% of the time, then that's where ALL of your efforts should go, but since that's not the case, you need to eliminate debt, secure housing for the rest of your life, and enter retirement with 3 YEARS of expenses liquid...could be in a savings account (even a high yield one), just a checking account earning no interest, or (not my choice) even CDs if you want...as long as you can get at the money if you need to pay bills if the stock market goes down a lot and you don't want to draw from it then.

4) An even better strategy is to invest MORE than the minimum so you can feel confident taking money from your very big pile in retirement even IF the market tanks for several years...BUT most people don't get there.

another too pessimistic market call from the bottom a year ago.

This poster suggested slapping a 10 or 12 PE on the SP500, to get it below 3000. It's above 4000 today.

Although to be fair he says if earnings expectations change so might his forecast.

AndreasStenoLarsen @AndreasSteno A Forward P/E of 10-12 seems justified given the most recent surge in real rates in USD That means S&P 500 <3000 on unchanged earnings assumptions.. Ouch

another too pessimistic market call from the bottom a year ago.

This poster suggested slapping a 10 or 12 PE on the SP500, to get it below 3000. It's above 4000 today.

Although to be fair he says if earnings expectations change so might his forecast.

AndreasStenoLarsen @AndreasSteno A Forward P/E of 10-12 seems justified given the most recent surge in real rates in USD That means S&P 500 <3000 on unchanged earnings assumptions.. Ouch

0:41 AM · Oct 31, 2022

ANY talk of market direction in the near term due to ANY normal economic condition (meaning not affected by war or some other non-economic anomaly of a thing) is just noise. If ONLY it were that easy. It's akin to Tarot Card Reading...might be fun for some, but it's nonsense.

This is 100% true, unless there is some rule about what the treasury can and cannot do. Not borrowing trillions and trillions at 1% was one of the largest financial blunders in world history, in terms of raw value lost. Yellen should be fired for it, if that was a conscious decision.

Frederik Gieschen @NeckarValue Stanley Druckenmiller on the Fed's historic blunder: "When rates were practically zero, every Tom, Dick and Harry and Mary in the United States refinanced their mortgage, corporations extended. Unfortunately, we've had one entity that did not and that was US Treasury. Janet Yellen, I guess, because of political myopia, whatever, was issuing two years at 15 basis points when she could have issued 10 years at 70 basis points, or 30 years at 180 basis points. I literally think if you go back to Alexander Hamilton, it was the biggest blunder in the history of the Treasury. I have no idea why she has not been called out on this. She has no right to still be in that job."

This post was edited 1 minute after it was posted.

This is 100% true, unless there is some rule about what the treasury can and cannot do. Not borrowing trillions and trillions at 1% was one of the largest financial blunders in world history, in terms of raw value lost. Yellen should be fired for it, if that was a conscious decision.

Frederik Gieschen @NeckarValue Stanley Druckenmiller on the Fed's historic blunder: "When rates were practically zero, every Tom, Dick and Harry and Mary in the United States refinanced their mortgage, corporations extended. Unfortunately, we've had one entity that did not and that was US Treasury. Janet Yellen, I guess, because of political myopia, whatever, was issuing two years at 15 basis points when she could have issued 10 years at 70 basis points, or 30 years at 180 basis points. I literally think if you go back to Alexander Hamilton, it was the biggest blunder in the history of the Treasury. I have no idea why she has not been called out on this. She has no right to still be in that job."

The entire construct of both the Fed and Treasury operations that period was very destructive. And the fallacy remains that balance sheet losses and printing away the costs has no consequences. Clearly that was never true.

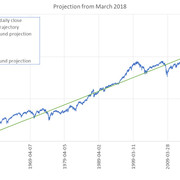

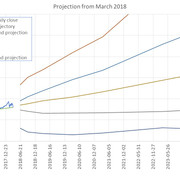

I thought I would revisit my March 2018 naive forecasts for SP500. As a reminder, I took the index since 1950, drew a simple best fit trend through the data, as representing a crude "mean" trend about which the index would fluctuate, then used observed fluctuations about that trend to establish forward-looking bounds on expected future trends, with a "most likely" trend and approximate 80% confidence interval for the then-future 8 years or so.

This is what the forecast looked like in March 2018, first showing the whole history since 1950, then looking more closely at the near future:

At the time, the forecast attracted ridicule for being less than useless, given the range in expected future values. That was (and remains) a fair criticism. That said, if we show the post-forecast actual data in the intervening 5 1/2 years, we see that actual behavior lined up pretty well with the forecast:

You can see that the index has indeed fluctuated about the median projection, and currently lies pretty close to it. I still think the index is most likely to be around 4600 by the end of 2025, but will almost certainly vary quite a bit along the way there, and could easily be quite a bit lower or higher. I have not updated the forward-looking projections since March 2018, but I suggest the index is almost certain (80% confidence) to lie between 3900 and 5400 at the end of 2025. And certain (99.9% confidence) to lie between 2900 (worst case crash) and 6400 (best case surprise bull run).

You'll note that this naive forecast takes no consideration of world events or other forces assumed to drive the markets, it is strictly data-driven.

This I've shared for free, which is probably exactly what it's worth. :-)

Maybe I'll just add how I've used this in my own investing. I've looked at this as a rough indication of overall market value. When the index has fluctuated well above the median projection, I've believed the SP500 to be "expensive" and when below the trend, "cheap," and made some investing decisions on that basis.

As the post-covid crash bull run progressed, I got more and more concerned about things being overheated and eventually stepped completely out of US index funds in the first half of 2021. That turned out initially to be a bad idea as the bull run continued, but eventually turned in my favor. Since I was coincidentally retiring in the then-near future, I took it as an opportunity to de-risk our portfolio, which created a very nice (and very lucky) opportunity to load up on fixed income products, more suited to our current risk tolerance and future money needs. This feels like it was smart, but I know it was mainly very lucky.

Maybe I'll just add how I've used this in my own investing. I've looked at this as a rough indication of overall market value. When the index has fluctuated well above the median projection, I've believed the SP500 to be "expensive" and when below the trend, "cheap," and made some investing decisions on that basis.

As the post-covid crash bull run progressed, I got more and more concerned about things being overheated and eventually stepped completely out of US index funds in the first half of 2021. That turned out initially to be a bad idea as the bull run continued, but eventually turned in my favor. Since I was coincidentally retiring in the then-near future, I took it as an opportunity to de-risk our portfolio, which created a very nice (and very lucky) opportunity to load up on fixed income products, more suited to our current risk tolerance and future money needs. This feels like it was smart, but I know it was mainly very lucky.

Sounds like a very prudent and wise decision given your retirement horizons being what they were. Congrats on that.

In fact, probably particularly opportune given the attractive yields available at the time (and currently) when you moved into fixed assets and the like.

Maybe I'll also add that the forecast I shared in 2018, with its very broad range of future possibilities, pretty much captures my philosophy about the markets. I happen to believe that they behave outside deterministic prediction, with no link between cause and effect, and that they make us all, even the experts, idiots when we try to make predictions, except in the broadest, most general forms (like that then-useless forecast). Like "predicting" that the markets have a 73% chance of ending any year higher than they started it.

I note that agip's steady drip of pi$$-poor expert predictions over the past couple of years really underscores my point. If the best educated, most experienced "experts" keep getting things so badly wrong so often, how could any of us be less idiotic?

Maybe I'll leave that question to hand out there for the philosophers... :-)

$NVDA CEO & President of NVIDIA Jensen Huang has cashed out over $42,000,000 in shares over the last week. Sold to you. Meanwhile the SOXS Igy bought two days ago up double digits.

A year ago a former GS CEO suggested that the universal gloom might unexpectedly lift and oct 2022 might be a good time to be a contrarian. And it was. US stocks rallied hard.

Lloyd Blankfein @lloydblankfein Seems EVERYONE negative on the mkt with sticky inflation, more rate hikes, other bad stuff ahead. Yet…inconceivable for all pundits to be right, but often all are wrong. Positives may be lurking. Fed pause, Ukraine truce, China lockdown end, etc. Sentiment can shift suddenly.

NEEDHAM, on last night's $AAPL event: "The odd timing, just 3 days before earnings, causes us to worry that laptop and iMac sales were weak in the Sept Q. That would suggest that last night's launch was a way to mitigate any negative share price reaction .."