“As the stock market rips in this Santa rally, nobody seems to have noticed that since the end of September, Q4 EPS estimates have been trimmed more than -5% and 2024 by -1%. Then again, who needs fundamentals when you have seasonals, momentum and a dovish Fed as tailwinds?”

NASDAQ closes the year up 44%. Just amazing. Best year since 2003. People who got out when things went south - sorry.

I heard that the individual investors as a class have been reluctant to get back in, and this is probably attributable to getting burned and the availability of other lucrative investment opportunities, like bonds and HYSA.

My bet is that this will gradually change and give strength to yet more gains in the market and Nasdaq.

Sally, some investors can exceed the SNP500 index benchmark over the long term. Trust me, they can. Maybe not most, maybe not during some short-term periods, etc., but some can exceed that benchmark overall.

Perhaps a more fruitful discussion would be to understand what distinct advantages has over an index portfolio and over large fund managers, in the goal of using those things to the individual investor's advantage.

If you are talking about financial advisors specifically, that is a different discussion, and Agip has started to delve into the broader scope of services and benefits of using one besides beating the SNP.

one of the fascinating problems advisors have is long periods like the current, when one sector - tech in this case - has wildly outperformed.

Advisors are going to diversify clients, because that's what you are supposed to do. Small caps, emerging, bonds of all kinds, value, etc.

Diversification is supposed to be the one free lunch. But in this case, of course, every share of anything other than tech stocks has contributed to underperformance. And this has gone on since what - 2010ish?

So advisors have hurt clients in an absolute return sense by doing the 'right' thing. Clients would have been better off for 10+ years to just own the sp500 and not have diversified portfolios. Book learning has done some real harm here.

I'm hoping this changes over the next 10 years and higher interest rates make investing more about cash flows and less about speculation.

I agree with you in a general sense, but wouldn't a financial advisor start with a diversified portfolio for a client, then tweak it based on the needs of the client?

Here's the thing - if a client said I want to risk it and all I care about is maximizing ROI, we might actually get outcomes where their returns outperformed the indices.

But we both know that this is unlikely because the advisor would do their very best to talk them out of it or just tell them that they (the advisor) can't help them.

And far more likely is that the advisor would, after reviewing their background (investment horizon, risk tolerance, financial buffers, etc.), would tweak their baseline portfolio to more of a "growth" bias - very much like what fund managers in the "growth" sector do, which is to assume a slight tech bias. And with a little luck, the result might outperform indices by a few percent (or trail it in down years).

In simple terms, if asked, I bet financial advisors don't see their principal function as beating the market indices. And there is probably the simple fact that most clients who could afford to, and want to, use a financial advisor are fairly risk averse and well off - both of which would make it more important to not lose money than to try to maximize gaining it.

one of the fascinating problems advisors have is long periods like the current, when one sector - tech in this case - has wildly outperformed.

Advisors are going to diversify clients, because that's what you are supposed to do. Small caps, emerging, bonds of all kinds, value, etc.

Diversification is supposed to be the one free lunch. But in this case, of course, every share of anything other than tech stocks has contributed to underperformance. And this has gone on since what - 2010ish?

So advisors have hurt clients in an absolute return sense by doing the 'right' thing. Clients would have been better off for 10+ years to just own the sp500 and not have diversified portfolios. Book learning has done some real harm here.

I'm hoping this changes over the next 10 years and higher interest rates make investing more about cash flows and less about speculation.

I agree with you in a general sense, but wouldn't a financial advisor start with a diversified portfolio for a client, then tweak it based on the needs of the client?

Here's the thing - if a client said I want to risk it and all I care about is maximizing ROI, we might actually get outcomes where their returns outperformed the indices.

But we both know that this is unlikely because the advisor would do their very best to talk them out of it or just tell them that they (the advisor) can't help them.

And far more likely is that the advisor would, after reviewing their background (investment horizon, risk tolerance, financial buffers, etc.), would tweak their baseline portfolio to more of a "growth" bias - very much like what fund managers in the "growth" sector do, which is to assume a slight tech bias. And with a little luck, the result might outperform indices by a few percent (or trail it in down years).

In simple terms, if asked, I bet financial advisors don't see their principal function as beating the market indices. And there is probably the simple fact that most clients who could afford to, and want to, use a financial advisor are fairly risk averse and well off - both of which would make it more important to not lose money than to try to maximize gaining it.

sure, a good advisor will tweak a portfolio to match each client. If a client wants more risk then the advisor could add risk and maybe get more return.

The problem is that the core problem stays...tech outperformance has been so massive for 10+ years that owning anything other than tech/SP500 has caused underperformance. Diversification has been a loser no matter if it's extreme or light.

SP500 is 30% tech. If you own small caps or value, a client will have less than that 30% and will underperform the Sp500. Add in bonds and a client gets no where near the SP500.

All of which is to say, so far, to this point, this is why indexing works so well. It has forced investors to own all that tech and that has been a great move.

NASDAQ closes the year up 44%. Just amazing. Best year since 2003. People who got out when things went south - sorry.

I heard that the individual investors as a class have been reluctant to get back in, and this is probably attributable to getting burned and the availability of other lucrative investment opportunities, like bonds and HYSA.

My bet is that this will gradually change and give strength to yet more gains in the market and Nasdaq.

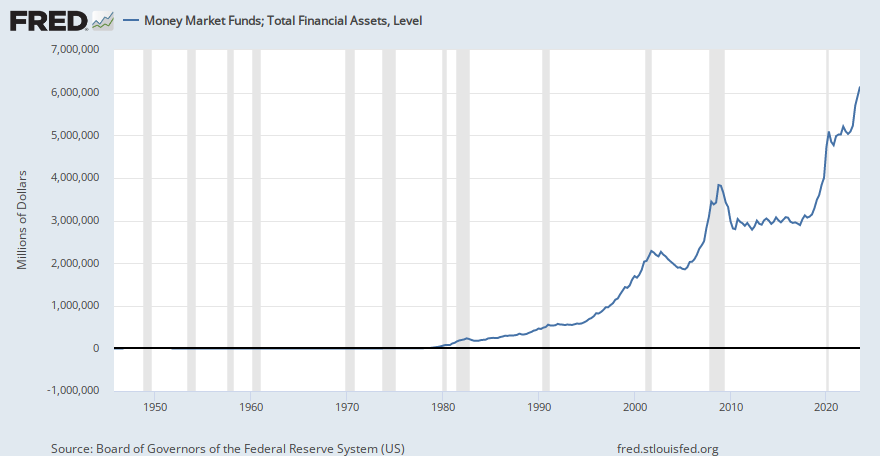

ja, the amount of cash in money markets 'waiting' is absolutely ginormous and still climbing sharply. if that moves to stocks....

I heard that the individual investors as a class have been reluctant to get back in, and this is probably attributable to getting burned and the availability of other lucrative investment opportunities, like bonds and HYSA.

My bet is that this will gradually change and give strength to yet more gains in the market and Nasdaq.

ja, the amount of cash in money markets 'waiting' is absolutely ginormous and still climbing sharply. if that moves to stocks....

For every stock bought, someone else sold. There is “no cash on the sidelines.” The only difference is eagerness to buy, fear of missing out; or eagerness to sell, fear of losing money.

Wall Street is once again pushing the feel-good theory that there is a giant wave of money just waiting to come into the stock market and drive stock prices...

I heard that the individual investors as a class have been reluctant to get back in, and this is probably attributable to getting burned and the availability of other lucrative investment opportunities, like bonds and HYSA.

My bet is that this will gradually change and give strength to yet more gains in the market and Nasdaq.

ja, the amount of cash in money markets 'waiting' is absolutely ginormous and still climbing sharply. if that moves to stocks....

Dude, it is going to move to stocks. Don't underestimate FOMO. Just wait until the press starts pumping those headlines about how good a run this is.... And it will feed itself for awhile....

That's in the short term. I still think there is something to the long term changing of the demographics, though, wherein shrinking population leads to less people feeding the markets, and I know that you have made mention of this in passing recently. That will be very long term, though, and I bet that plays out with just more modest bull runs years hence.

This makes no sense to me. His premise: "So any individual can “put their cash to work” by investing in stocks. But individuals in total can’t do so. This is a basic logical fallacy, the fallacy of composition."

BS. It ignores turn over rate (what if instead of cash being on the sidelines months waiting to be reinvested, it is only there days or hours, and if so, prices fly higher faster!), and new issues, and the money going into actual equities and out of safe heaven stocks, etc.

Increase demand, stocks go up. I can't see how that eludes anyone.

* the heart of his mistake is that he thinks it is a closed system. It is not. The money comes out of bonds, real estate, money market funds, CDs, etc., and instead get thrown into stocks. Consequently, the stock market goes up, but those fixed income investments go down.

See, he is right if you consider it within the whole spectrum of investment vehicles. But he is wrong to think that stocks cannot go up while the others go down.

This makes no sense to me. His premise: "So any individual can “put their cash to work” by investing in stocks. But individuals in total can’t do so. This is a basic logical fallacy, the fallacy of composition."

BS. It ignores turn over rate (what if instead of cash being on the sidelines months waiting to be reinvested, it is only there days or hours, and if so, prices fly higher faster!), and new issues, and the money going into actual equities and out of safe heaven stocks, etc.

Increase demand, stocks go up. I can't see how that eludes anyone.

So when the cash is “on the sidelines,” who is holding the stocks?

This makes no sense to me. His premise: "So any individual can “put their cash to work” by investing in stocks. But individuals in total can’t do so. This is a basic logical fallacy, the fallacy of composition."

BS. It ignores turn over rate (what if instead of cash being on the sidelines months waiting to be reinvested, it is only there days or hours, and if so, prices fly higher faster!), and new issues, and the money going into actual equities and out of safe heaven stocks, etc.

Increase demand, stocks go up. I can't see how that eludes anyone.

So when the cash is “on the sidelines,” who is holding the stocks?

It's a basic auction system, investors bid and demand determines the price of the transaction.

More demand raises the price, and demand increases as money moves from one part of the system (bonds, money market, etc.) and into the in-demand part of the system: stocks.

Again, his fallacy is to disregard that the other parts of the closed system which will move in equilibrium by going down, and that is the sectors like bonds and money markets.

This is what happens in reality, and is plainly obvious. So obvious in fact, that it might be overlooked.

“Again, his fallacy is to disregard that the other parts of the closed system which will move in equilibrium by going down, and that is the sectors like bonds and money markets.”

There are no fewer bonds or money market once the “cash leaves the sidelines.” Those assets don’t just go into hibernation. Besides all stock trades are settled in cash, making that argument largely nonsense. Stocks bought, equal amount goes to the seller, and “back on the sidelines.” The only potential variable here is a more eager buyer, and certainly Wall Street is spinning the “cash on the sidelines” narrative to encourage business.

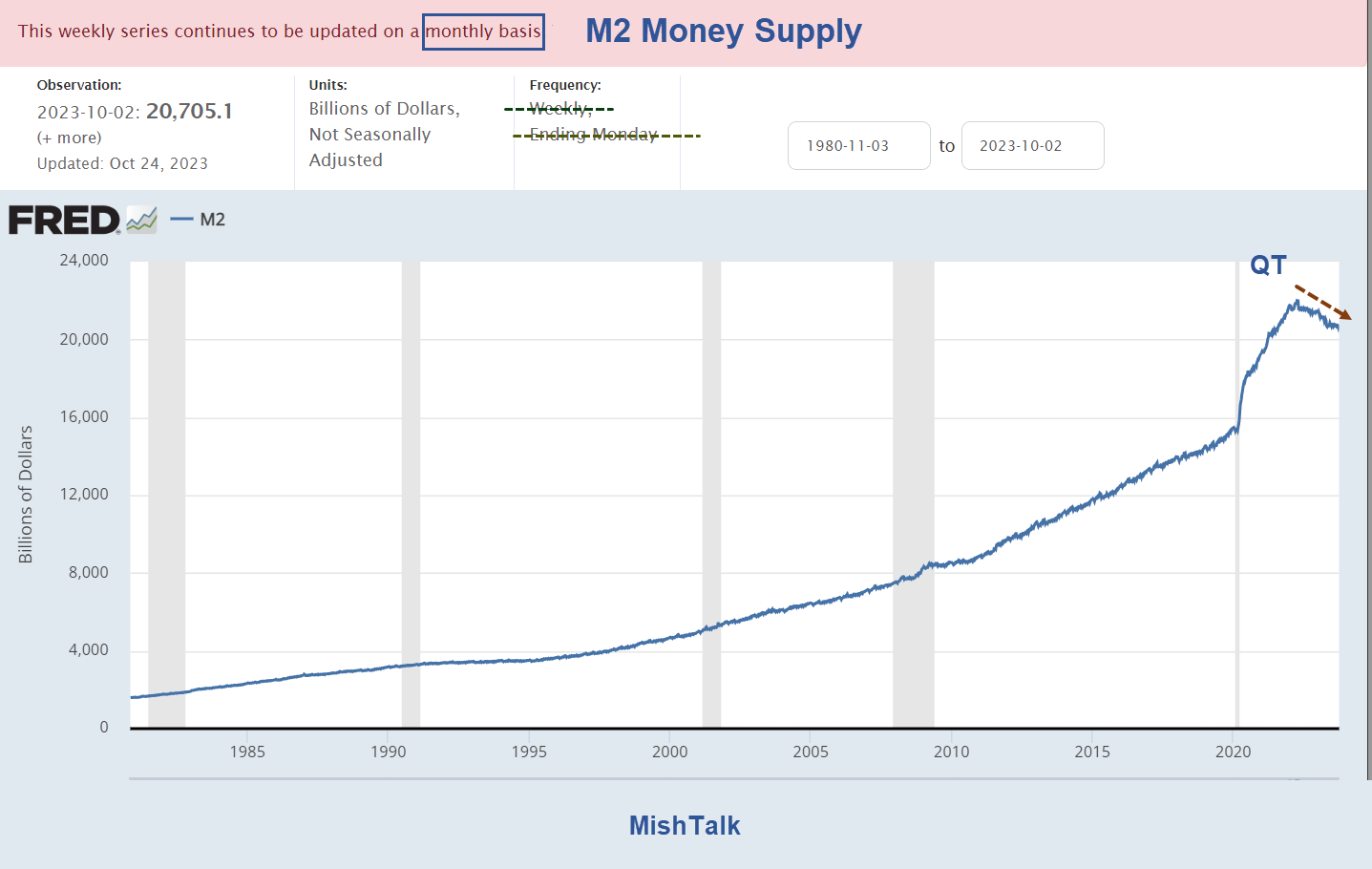

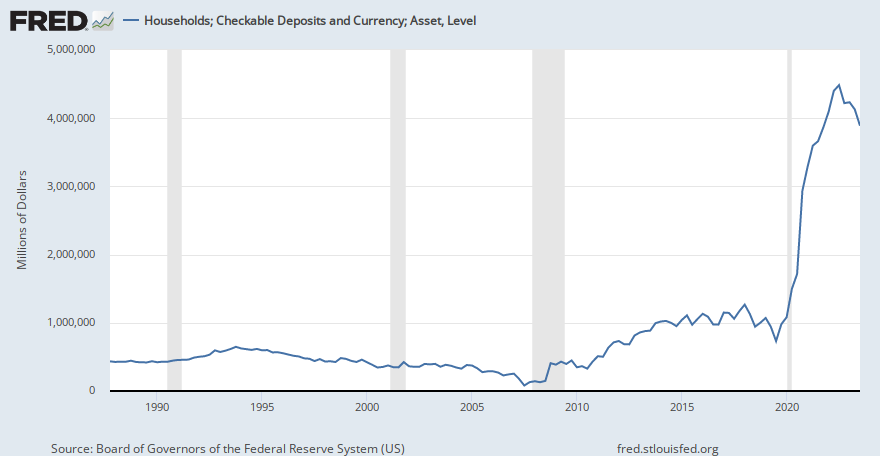

Granted agip’s money market chart shows rising balances, but represents funds flows from low interest checking to money market. One of the main reasons regional banks ran into problems (capital requirements to back lending; that and purchasing long dated securities in a reach for yield, no longer liquid with falling values) as customers moved money out of checking into money markets at investment firms. So that entire narrative is rather foolish. Bullish nonsense.

Help us build the best running shoe review site for a chance to win a LetsRun t-shirt.Help us build the best running shoe review site for a chance to win one of 10 LetsRun t-shirts.